The steel industry’s carbon conundrum

The Steel Decarbonization Dynamics Service (SDDS) is a comprehensive intelligence platform built around the global steel industry’s decarbonization challenge. It combines in-depth analysis, proprietary forecasting and customizable modeling with outlooks extending to 2030, 2040 and beyond. What sets SDDS apart from the growing volume of decarbonization research:

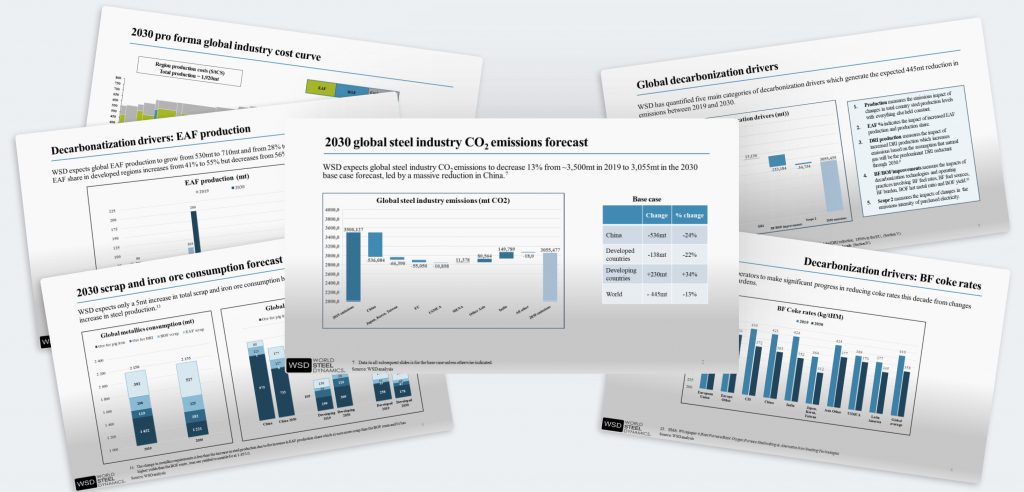

Grounded in reality, not aspiration. SDDS focuses on what is likely to happen — not what could or should. Every forecast is built on the economics, politics and technical constraints that will actually shape the transition.

A fully integrated model. Our proprietary framework links CO2 emissions, cost structures, raw material balances and energy requirements into a single, internally consistent view — so subscribers can see how a change in one variable ripples across the others.

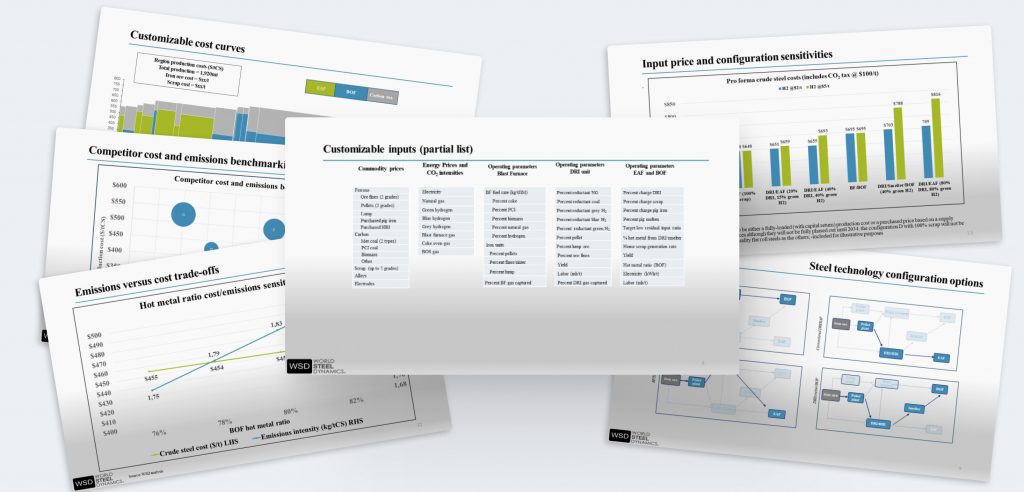

Scenario planning in your hands. The platform lets users build custom scenarios by adjusting hundreds of inputs at the country, region and plant level, turning our model into a tool tailored to your specific strategic questions.

SDDS reflects WSD’s decades-long commitment to rigorous, independent analysis — including the conclusions others are reluctant to draw.

WSD is available for customized presentation, consultation with your Board of Directors, Management Team, etc. Schedule a call today for more information